Updated June 2026

What Is Collision Coverage Insurance?

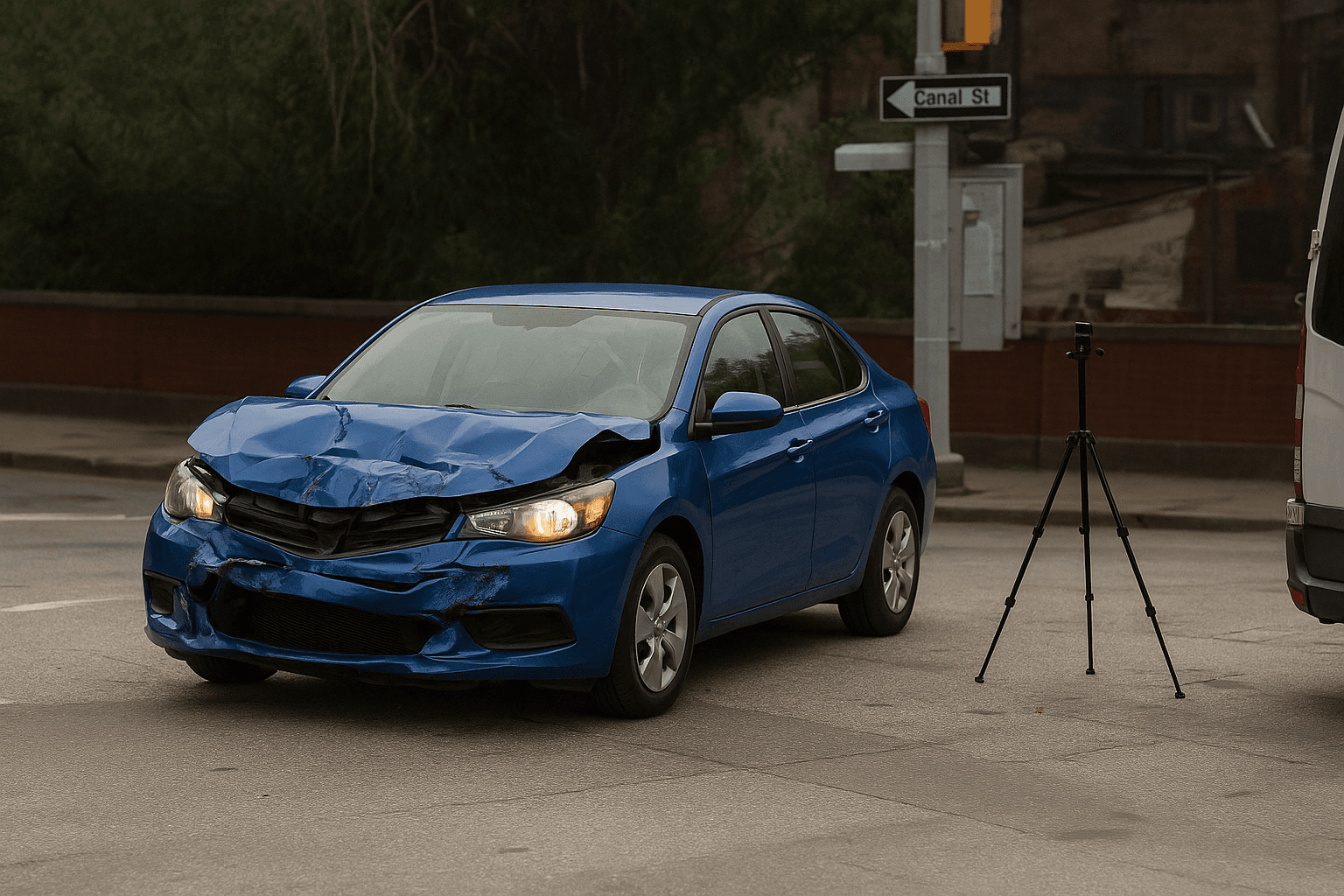

Collision coverage pays to repair or replace your vehicle when it's damaged in an accident with another vehicle or object, or when it rolls over in a single-car crash. Unlike liability coverage, which pays for damage you cause to someone else's property, collision pays for your own vehicle regardless of who was at fault. The insurer pays up to the actual cash value of the car minus your chosen deductible. If repair costs exceed the car's depreciated market value, the insurer declares it a total loss and pays you that value instead of fixing it.

- You're driving on the Thruway and don't brake in time, rear-ending the car ahead at a stoplight. Your front bumper, hood, and radiator suffer $4,200 in damage. The other driver's car has $3,800 in damage and they have $6,500 in medical bills. Your liability coverage pays the other driver's $10,300 in total costs. Your collision coverage pays the $4,200 to fix your car, minus your $500 deductible — you receive $3,700. Without collision, you pay the full $4,200 out of pocket.

- You swerve to avoid debris on Route 17 and strike a guardrail, causing $7,800 in damage to your vehicle. No other car is involved. Your collision coverage pays to repair your car up to its actual cash value, minus your deductible. If your car is worth $9,000 and you carry a $1,000 deductible, you receive $6,800. If the car is worth only $6,500, the insurer totals it and pays you $5,500 after the deductible. Liability coverage pays nothing because no other party was damaged.

- Another driver runs a red light and T-bones your car, causing $5,200 in damage. The other driver has no insurance and no assets to sue for. Your collision coverage pays the $5,200 minus your $500 deductible. You can then file a claim under your uninsured motorist property damage coverage to recover the $500 deductible in some cases, depending on your policy. Without collision, you'd have to sue the uninsured driver directly and collect nothing if they have no money.

Who Needs Collision Coverage Insurance?

Collision coverage makes sense if your car is worth more than ten times the annual premium, you're still making loan or lease payments, or you don't have $5,000 to $15,000 saved to replace the car out of pocket after a total loss. Retirees who recently bought a newer vehicle or who drive in high-traffic areas where accident risk remains elevated should keep collision until the car's value drops below the threshold where self-insuring becomes cheaper.

Calculate your car's current actual cash value using Kelley Blue Book or NADA. Multiply your annual collision premium by three. If three years of premiums exceed the car's value, or if the car is worth less than $6,000 and you have savings to replace it, dropping collision usually makes financial sense. If you're unsure, raise your deductible to $1,000 or $2,000 to lower the premium while keeping catastrophic protection in place.

How Much Does Collision Coverage Insurance Cost?

Collision coverage typically adds $30 to $70 per month to a New York auto policy, or $360 to $840 annually, depending on the car's value, your deductible, and your driving record.

- Vehicle age and depreciated market value — a 2018 sedan valued at $12,000 costs less to insure for collision than a 2023 SUV valued at $35,000.

- Chosen deductible — selecting a $1,000 deductible instead of $500 can lower your premium by 15 to 25 percent, but you pay more out of pocket per claim.

- Driving record and claims history — a single at-fault accident in the past three years can raise collision premiums by 20 to 40 percent in New York.

- Garage location and theft rates — cars garaged in New York City boroughs pay higher collision premiums than those in rural upstate counties due to accident frequency and repair costs.

- Annual mileage — drivers logging under 7,500 miles per year, common among retirees, may qualify for low-mileage discounts that reduce collision costs by 10 to 20 percent with carriers like Metromile or Nationwide.